How to

20x

the world’s largest

capital markets

Real Estate

Renewables

Infrastructure

How to

20x

the world’s largest

capital markets

Real Estate

Renewables

Infrastructure

How to

20x

the world’s largest

capital markets

Real Estate

Renewables

Infrastructure

Background

This paper presents a thought experiment to identify the most valuable use of technology in financing markets for renewable energy, real estate, and infrastructure.

We aim to convince you that there is an optimal leverage point for technology to drive dramatic growth in the massive, opaque markets for clean energy, real estate, and infrastructure.

These conclusions have formed the bedrock of our company, Phosphor.

Background

This paper presents a thought experiment to identify the most valuable use of technology in financing markets for renewable energy, real estate, and infrastructure.

We aim to convince you that there is an optimal leverage point for technology to drive dramatic growth in the massive, opaque markets for clean energy, real estate, and infrastructure.

These conclusions have formed the bedrock of our company, Phosphor.

Background

This paper presents a thought experiment to identify the most valuable use of technology in financing markets for renewable energy, real estate, and infrastructure.

We aim to convince you that there is an optimal leverage point for technology to drive dramatic growth in the massive, opaque markets for clean energy, real estate, and infrastructure.

These conclusions have formed the bedrock of our company, Phosphor.

Prelude: Solving all the wrong problems

Renewables, real estate, real assets.

At first glance, office towers in New York bear little resemblance to mini-grids in West Africa.

But beneath the surface, similarities form: we find a set of interdependent rules and obligations encoded legally in contracts and financial models, which describe how cash flows between parties and under what conditions.

These rules create a legal foundation through which the built world is financed: real assets.

When investing in a solar project, we invest in a real asset. When we take out a mortgage for an apartment complex, we do so against a real asset.

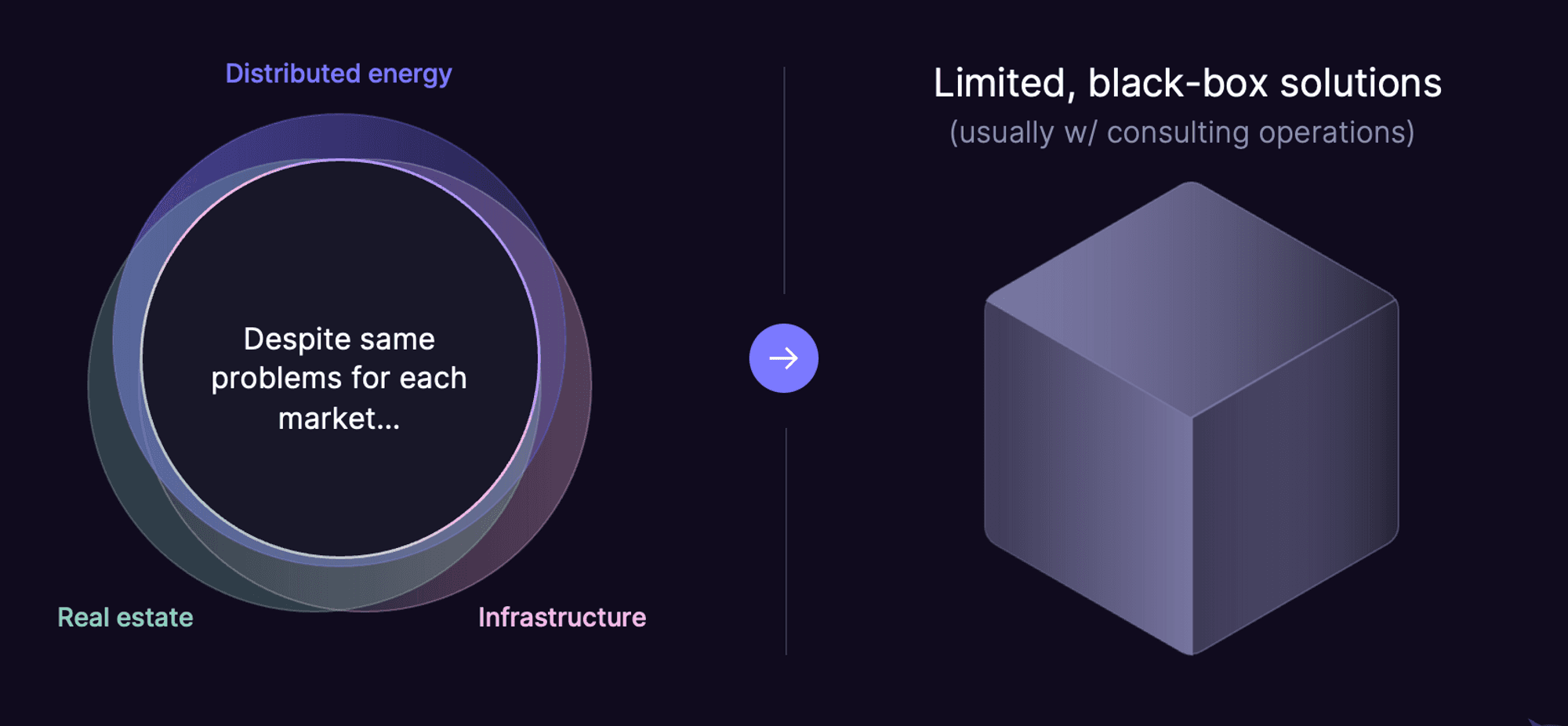

Real asset markets (institutional real estate, renewables, etc.) — worth trillions of dollars — are grossly inefficient. To date, attempts to improve efficiency have focused narrowly on specific markets (e.g. “project finance” software for solar, or “automated valuation models” for real estate).

Despite the same foundational problems across these markets, nobody has figured out how to create a holistic, transformative solution: attempts have built around frays of the problem, leading to limited solutions that often require extensive consulting services.

At first glance, office towers in New York bear little resemblance to mini-grids in West Africa.

But beneath the surface, similarities form: we find a set of interdependent rules and obligations encoded legally in contracts and financial models, which describe how cash flows between parties and under what conditions.

These rules create a legal foundation through which the built world is financed: real assets.

When investing in a solar project, we invest in a real asset. When we take out a mortgage for an apartment complex, we do so against a real asset.

Real asset markets (institutional real estate, renewables, etc.) — worth trillions of dollars — are grossly inefficient. To date, attempts to improve efficiency have focused narrowly on specific markets (e.g. “project finance” software for solar, or “automated valuation models” for real estate).

Despite the same foundational problems across these markets, nobody has figured out how to create a holistic, transformative solution: attempts have built around frays of the problem, leading to limited solutions that often require extensive consulting services.

Why is this so hard? What is this problem which has gone so completely misidentified?

Identifying it took us years. It’s only easy to identify in reverse because if we examine it sequentially, we would reproduce the same blindspots as everyone else.

This paper starts with an end goal: the largest market in the world, radically transformed in size. We walk backward through three critical steps to uncover the broken links in a long dependency chain which we believe hold the keys to dramatic market transformation.

Identifying it took us years. It’s only easy to identify in reverse because if we examine it sequentially, we would reproduce the same blindspots as everyone else.

This paper starts with an end goal: the largest market in the world, radically transformed in size. We walk backward through three critical steps to uncover the broken links in a long dependency chain which we believe hold the keys to dramatic market transformation.

Step III: Drive a huge shift in liquidity

Exponential market growth occurs when the ability to trade a given asset for cash becomes faster and easier. In finance-speak, this is referred to as liquidity, which is most easily understood as a measure of “buyer’s remorse”.

If I buy stock in a company and can easily change my mind and resell it for the same amount, the market is liquid. If I have no marketplace or no easy way to resell it without losing value, it’s illiquid, and I’m stuck “holding the bag”.

Real asset markets are among the most illiquid markets in all of finance. This section explores the impact we stand to make by making them liquid and why they’re illiquid in the first place.

Exponential market growth occurs when the ability to trade a given asset for cash becomes faster and easier. In finance-speak, this is referred to as liquidity, which is most easily understood as a measure of “buyer’s remorse”.

If I buy stock in a company and can easily change my mind and resell it for the same amount, the market is liquid. If I have no marketplace or no easy way to resell it without losing value, it’s illiquid, and I’m stuck “holding the bag”.

Real asset markets are among the most illiquid markets in all of finance. This section explores the impact we stand to make by making them liquid and why they’re illiquid in the first place.

How reducing “buyer’s remorse” drives impact

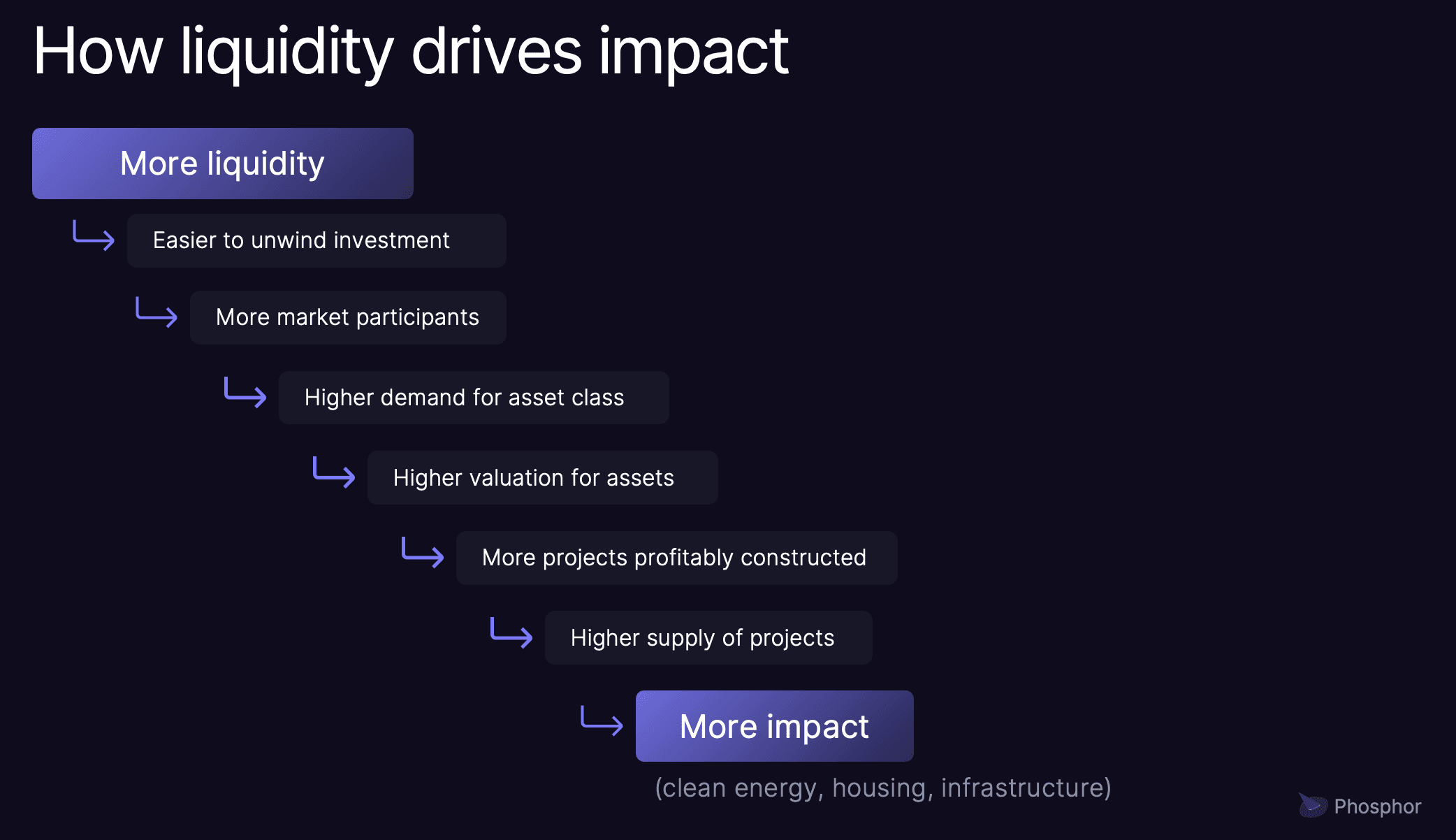

We care about liquidity because when it increases, the impact is exponential:

We care about liquidity because when it increases, the impact is exponential:

The most exciting prospect of improving market conditions lies in how linear increases to liquidity unlock non-linear market growth in project development (e.g. renewables, infrastructure, or housing).

Non-linearity occurs because projects are only constructed when the value of their expected cash flows exceeds the cost to build them. This is a game of margins, which means that when heightened market demand provides a higher valuation to the same set of cash flows, valuation improvements for projects which couldn’t previously be constructed may now do so profitably. Of course, the impact of housing or clean energy is only imparted when built.

The opportunity to "unlock liquidity" in these markets is enormous: the estimated global value of renewables, infrastructure, and real estate combined, exceeds $327 trillion, with only ~$11 trillion of it actually liquid (via public markets).

Relativity tends to make these numbers seem smaller than they are. For reference, one trillion dollars looks like this: $1,000,000,000,000.

The most exciting prospect of improving market conditions lies in how linear increases to liquidity unlock non-linear market growth in project development (e.g. renewables, infrastructure, or housing).

Non-linearity occurs because projects are only constructed when the value of their expected cash flows exceeds the cost to build them. This is a game of margins, which means that when heightened market demand provides a higher valuation to the same set of cash flows, valuation improvements for projects which couldn’t previously be constructed may now do so profitably. Of course, the impact of housing or clean energy is only imparted when built.

The opportunity to "unlock liquidity" in these markets is enormous: the estimated global value of renewables, infrastructure, and real estate combined, exceeds $327 trillion, with only ~$11 trillion of it actually liquid (via public markets).

Relativity tends to make these numbers seem smaller than they are. For reference, one trillion dollars looks like this: $1,000,000,000,000.

What illiquidity looks like in a real asset transaction

Complex investments (like real assets) require substantial amounts of time and effort to build confidence that an investment will perform as expected.

This confidence-building is called underwriting. Doing it well requires the three enemies of a liquid market: time, cost, and expertise. The more complex an asset class is, the more illiquid it will be.

Complex investments (like real assets) require substantial amounts of time and effort to build confidence that an investment will perform as expected.

This confidence-building is called underwriting. Doing it well requires the three enemies of a liquid market: time, cost, and expertise. The more complex an asset class is, the more illiquid it will be.

An illustrative example

Imagine that you're a professional solar investor. You'd like to invest in a solar project (… a real asset investment!).

The project you're buying has already been "developed," which means a developer has put key contracts in place and done preliminary design and engineering work, but it has not been constructed.

The outputs of this development work are the assumptions you'll build into a financial model to determine how much you can pay for this project based on a target return.

You'll often negotiate with the seller off of a shared, limited version of this model while privately keeping your financing assumptions (which guide your initial price) in an internal file.

Ensuring these models tie together is often a copy/paste process: you'll likely make dumb mistakes that throw your numbers off, even if you're very good at this.

Imagine that you're a professional solar investor. You'd like to invest in a solar project (… a real asset investment!).

The project you're buying has already been "developed," which means a developer has put key contracts in place and done preliminary design and engineering work, but it has not been constructed.

The outputs of this development work are the assumptions you'll build into a financial model to determine how much you can pay for this project based on a target return.

You'll often negotiate with the seller off of a shared, limited version of this model while privately keeping your financing assumptions (which guide your initial price) in an internal file.

Ensuring these models tie together is often a copy/paste process: you'll likely make dumb mistakes that throw your numbers off, even if you're very good at this.

😳

😳

Excel costs $30 a month. Excel models can cost $200,000+.

Software is often evaluated based on its function, but for these complex markets, it is substantially less valuable than the knowledge encoded within it.

It's important not to confuse this know-how with data: it'd be apt to think of a model purchase as incredibly expensive no-code software where the formulas are the end result, and Excel is the no-code system.

The acquisition agreements your lawyer drafts will heavily rely on the shared model: it is as much of a legal exhibit to a closing as the contracts themselves.

The acquisition agreements your lawyer drafts will heavily rely on the shared model: it is as much of a legal exhibit to a closing as the contracts themselves.

The diligence process

The price you negotiate with the developer usually assumes that the project can legally operate over a long period of time. Ensuring that this long-term view holds up is critical to holding together the model’s assumptions. For confidence, you’ll need to diligence hundreds of pages of contracts (and technical docs) to ensure no loopholes or mistakes are present.

Usually, you have two options: expensive advisors (lawyers, engineers, etc.) who will review the docs while providing strong strategic counsel for oodles of money, or mediocre ones who will miss crucial elements which will likely be discovered when you try to raise financing against the project. You will need to catch them ahead of time to avoid blowing up your return targets.

The price you negotiate with the developer usually assumes that the project can legally operate over a long period of time. Ensuring that this long-term view holds up is critical to holding together the model’s assumptions. For confidence, you’ll need to diligence hundreds of pages of contracts (and technical docs) to ensure no loopholes or mistakes are present.

Usually, you have two options: expensive advisors (lawyers, engineers, etc.) who will review the docs while providing strong strategic counsel for oodles of money, or mediocre ones who will miss crucial elements which will likely be discovered when you try to raise financing against the project. You will need to catch them ahead of time to avoid blowing up your return targets.

🏛️

🏛️

Senior legal advisors enjoy low-level diligence work as much as senior finance professionals enjoy doing analyst work.

Often, they have to do it in order to provide good counsel, craft effective documentation, and manage a tight closing timeline.

Assuming that the model’s assumptions hold after extensive diligence, you close on the price you negotiated with the developer and fund the project’s construction.

It takes enormous work to ensure that your valuation is accurate and that the project holds together. Once you’re signed, reselling this investment would require someone else to perform the same extensive diligence process.

None of this is romantic.

Yet, this is what financing renewable energy, infrastructure, or housing looks like in real life.

Assuming that the model’s assumptions hold after extensive diligence, you close on the price you negotiated with the developer and fund the project’s construction.

It takes enormous work to ensure that your valuation is accurate and that the project holds together. Once you’re signed, reselling this investment would require someone else to perform the same extensive diligence process.

None of this is romantic.

Yet, this is what financing renewable energy, infrastructure, or housing looks like in real life.

The redundant work problem

Solar is the least complex asset class in energy.

Yet, even for experienced solar investors, months are spent developing, reviewing, and negotiating things completely from scratch.

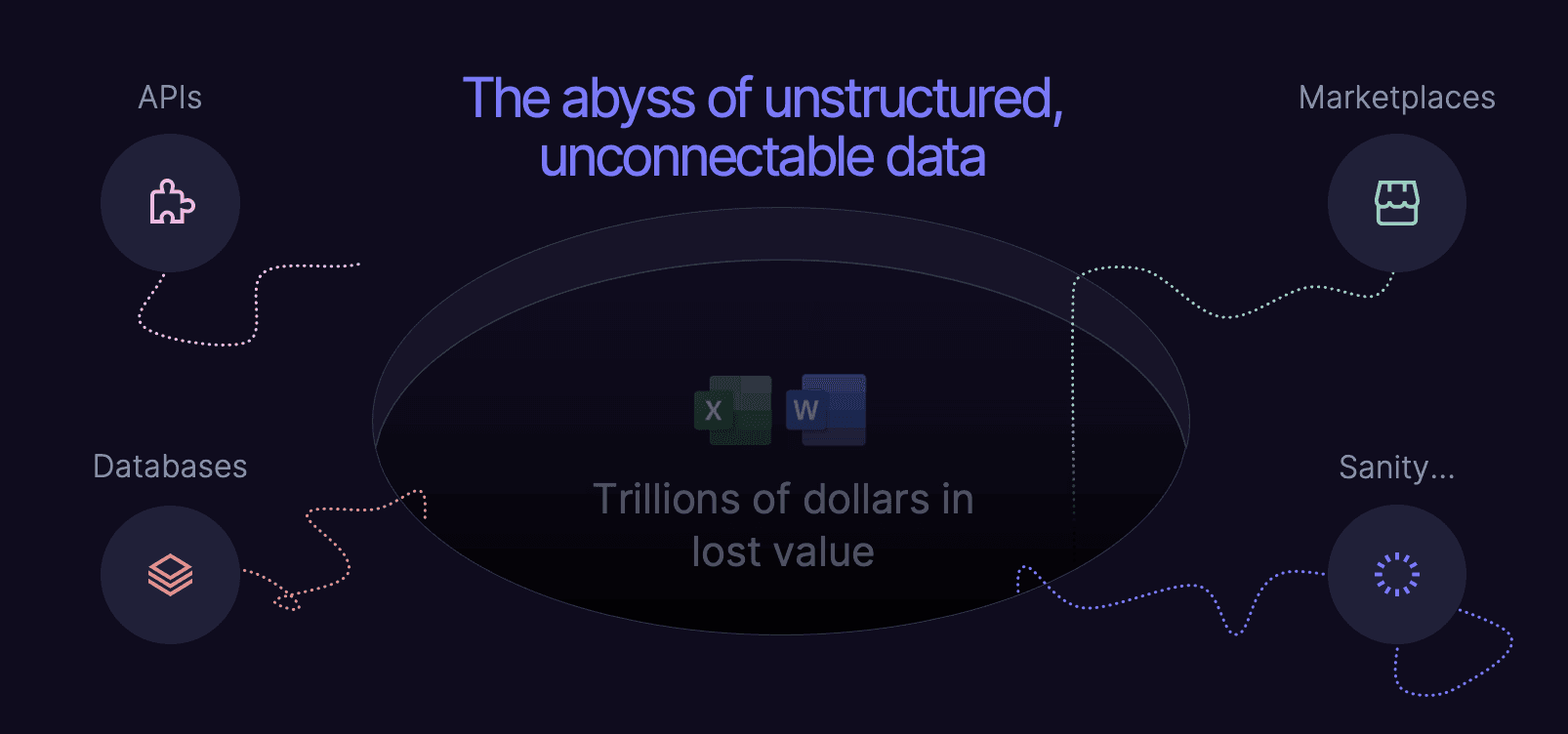

The two foundational exhibits of an investment — Excel and Word — can’t connect to outside data systematically despite almost every assumption being derived from a third-party system that likely has an API.

This lack of connectivity is where automation at scale breaks down.

Solar is the least complex asset class in energy.

Yet, even for experienced solar investors, months are spent developing, reviewing, and negotiating things completely from scratch.

The two foundational exhibits of an investment — Excel and Word — can’t connect to outside data systematically despite almost every assumption being derived from a third-party system that likely has an API.

This lack of connectivity is where automation at scale breaks down.

These same processes (and problems) apply to commercial real estate, wind power, toll roads, hospital buildings, etc., but often with much more time and cost, furthering the difficulties in financing the impact of this infrastructure.

How is it that for something as conceptually templated as a solar project, we have no basic means to re-apply knowledge that we’ve already developed?

At scale, enabling the reuse of work and knowledge (which costs the market over $100b per year) would transform how markets grow.

But what would that even look like?

These same processes (and problems) apply to commercial real estate, wind power, toll roads, hospital buildings, etc., but often with much more time and cost, furthering the difficulties in financing the impact of this infrastructure.

How is it that for something as conceptually templated as a solar project, we have no basic means to re-apply knowledge that we’ve already developed?

At scale, enabling the reuse of work and knowledge (which costs the market over $100b per year) would transform how markets grow.

But what would that even look like?

Step II: Eliminate complexity through standardization

Standardization — the coalescence of a market around a baseline of knowledge — is touted as a panacea for eliminating these redundancies.

But as we’ll see, the technology we define and negotiate an asset through creates enormous implementation challenges at the degree required for market-scale impact.

Standardization — the coalescence of a market around a baseline of knowledge — is touted as a panacea for eliminating these redundancies.

But as we’ll see, the technology we define and negotiate an asset through creates enormous implementation challenges at the degree required for market-scale impact.

“The greatest success story in modern economic history”

The scale of many of today’s most prominent financial markets can be traced directly to a standardization event: a point in time when market participants coalesced around a common set of rules and documents to define the sale or purchase of a given asset.

The most remarkable of these events occurred in 1987 when the world’s leading financial institutions formed the International Swaps and Derivatives Association (ISDA).

ISDA created a master agreement which, with buy-in from the market, became the backbone for interest rate swaps and derivatives. To the layman, these are big and scary names for conceptually simple assets where a party may transfer the interest rate risk of an investment (e.g., a “hedge”) to another counterparty (usually for a fee).

The scale of many of today’s most prominent financial markets can be traced directly to a standardization event: a point in time when market participants coalesced around a common set of rules and documents to define the sale or purchase of a given asset.

The most remarkable of these events occurred in 1987 when the world’s leading financial institutions formed the International Swaps and Derivatives Association (ISDA).

ISDA created a master agreement which, with buy-in from the market, became the backbone for interest rate swaps and derivatives. To the layman, these are big and scary names for conceptually simple assets where a party may transfer the interest rate risk of an investment (e.g., a “hedge”) to another counterparty (usually for a fee).

🚀

🚀

The ISDA standardization drove >1200x market growth for these already enormous markets. Historians describe it as “the greatest success story in modern economic history.”

Standardization breaks down for real assets

Unlike markets described above, real assets are composed of networks of contracts across numerous parties: to truly achieve the impact of standardization for a real asset, each of the various agreements would need standardizing across multiple markets.

While the contracts which underpin these assets have similar risks at the network level (e.g., the whole asset), these risks are allocated in all kinds of ways at the agreement level.

For example, a Power Purchase Agreement may double as a Lease Agreement where the power off-taker provides the land or a rooftop to install the site. This would combine off-take risk and site control risk into a single document.

The project developer may also provide EPC services (engineering, equipment procurement, and construction) as part of the sales agreement to a PE fund: this would combine market risk with engineering/execution risk.

The concepts within these agreements are often similar, but where they sit, and between whom makes the "look ma, no hands" implementation of a standard almost impossible without limiting it's scope, which largely defeats the point.

To complicate things further, real asset investments are often negotiated through shared financial models which become central exhibits to a closing. This enables contracts to defer a large amount of work to the model’s mechanics.

Unlike markets described above, real assets are composed of networks of contracts across numerous parties: to truly achieve the impact of standardization for a real asset, each of the various agreements would need standardizing across multiple markets.

While the contracts which underpin these assets have similar risks at the network level (e.g., the whole asset), these risks are allocated in all kinds of ways at the agreement level.

For example, a Power Purchase Agreement may double as a Lease Agreement where the power off-taker provides the land or a rooftop to install the site. This would combine off-take risk and site control risk into a single document.

The project developer may also provide EPC services (engineering, equipment procurement, and construction) as part of the sales agreement to a PE fund: this would combine market risk with engineering/execution risk.

The concepts within these agreements are often similar, but where they sit, and between whom makes the "look ma, no hands" implementation of a standard almost impossible without limiting it's scope, which largely defeats the point.

To complicate things further, real asset investments are often negotiated through shared financial models which become central exhibits to a closing. This enables contracts to defer a large amount of work to the model’s mechanics.

💳

This is completely different from how most industries use financial models: in a complex transaction, models are legal artifacts that underpin the economics and adjustment mechanisms of a deal.

The importance of ensuring the model’s correctness underpins an >$8b per year audit and consulting market.

From a technical perspective, it’s hard to imagine how standard documentation could be meaningful when so much relies on a tool whose language (=A5*B9) is meaningless and can’t be standardized or directly linked to a contract in the first place.

Where do we even go from here?

From a technical perspective, it’s hard to imagine how standard documentation could be meaningful when so much relies on a tool whose language (=A5*B9) is meaningless and can’t be standardized or directly linked to a contract in the first place.

Where do we even go from here?

Back to first principles

In the prelude, we described an asset as a set of “rules” encoded into contracts and financial models.

By driving a wedge between what a rule is, versus how or where it gets encoded, we create space to identify where this information loses structure in the first place.

Isn't it odd that these rules aren’t computer-friendly?

In the prelude, we described an asset as a set of “rules” encoded into contracts and financial models.

By driving a wedge between what a rule is, versus how or where it gets encoded, we create space to identify where this information loses structure in the first place.

Isn't it odd that these rules aren’t computer-friendly?

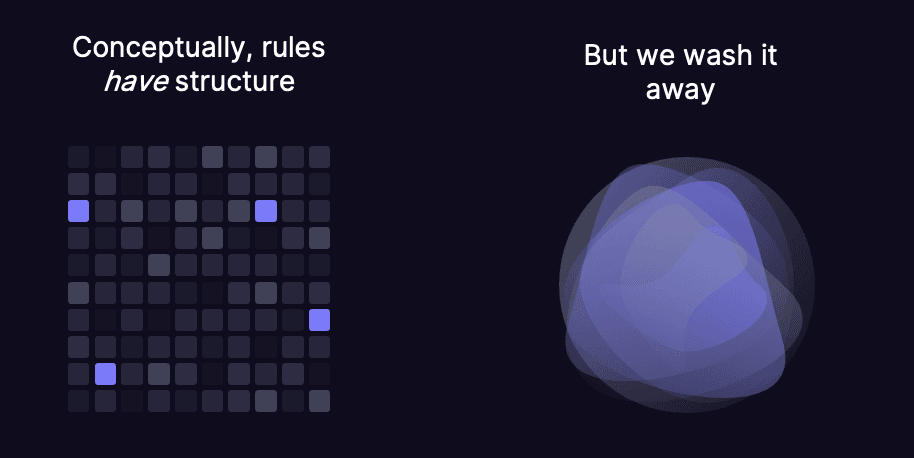

By their very nature, rules have inherent, logical structures, enabling them to compose obligations into large dependency graphs (e.g., contract terms). This structure gets washed away in the static text format of Microsoft Word or PDF docs.

We’re doing this wrong.

Losing this structure means our only credible opportunity to automate underwriting is via AI models which attempt to reassemble this structure.

We’ve taken the computer-friendly concepts of rules and logic, washed them away like a sand castle, and now pin our hopes on probabilistic models to put this structure back together when the structure should never be lost in the first place.

The AI road will dead-end.

By nature, AI models are probabilistic: they lack certainty, consistency, and predictability.

This means there will never be a path to truly automating underwriting work without a tradeoff between incurring undue risk or requiring manual review.

This inability to confidently and consistently make sense of unstructured data prevents the growth and transformation which might be achievable with end-to-end automation.

There is a single way to fix this.

By their very nature, rules have inherent, logical structures, enabling them to compose obligations into large dependency graphs (e.g., contract terms). This structure gets washed away in the static text format of Microsoft Word or PDF docs.

We’re doing this wrong.

Losing this structure means our only credible opportunity to automate underwriting is via AI models which attempt to reassemble this structure.

We’ve taken the computer-friendly concepts of rules and logic, washed them away like a sand castle, and now pin our hopes on probabilistic models to put this structure back together when the structure should never be lost in the first place.

The AI road will dead-end.

By nature, AI models are probabilistic: they lack certainty, consistency, and predictability.

This means there will never be a path to truly automating underwriting work without a tradeoff between incurring undue risk or requiring manual review.

This inability to confidently and consistently make sense of unstructured data prevents the growth and transformation which might be achievable with end-to-end automation.

There is a single way to fix this.

Step I: Rebuild the market’s linguistics

"Unstructured data" is practically synonymous with MS Word and Excel. This concern is often presented as a software problem.

But the real problem lies one step deeper: linguistics.

Computers can't handle ambiguity well. Programming languages that guide computers are constrained subsets of natural language. These constraints reduce ambiguity from natural language to enable a computer to compile to low-level machine instructions.

When language is ambiguous, compilation fails: the instructions are unclear.

To a computer, both Excel's cell reference language and the natural language of contracts are ambiguous beyond the files they're used within. They can't be compared by or connected to anything.

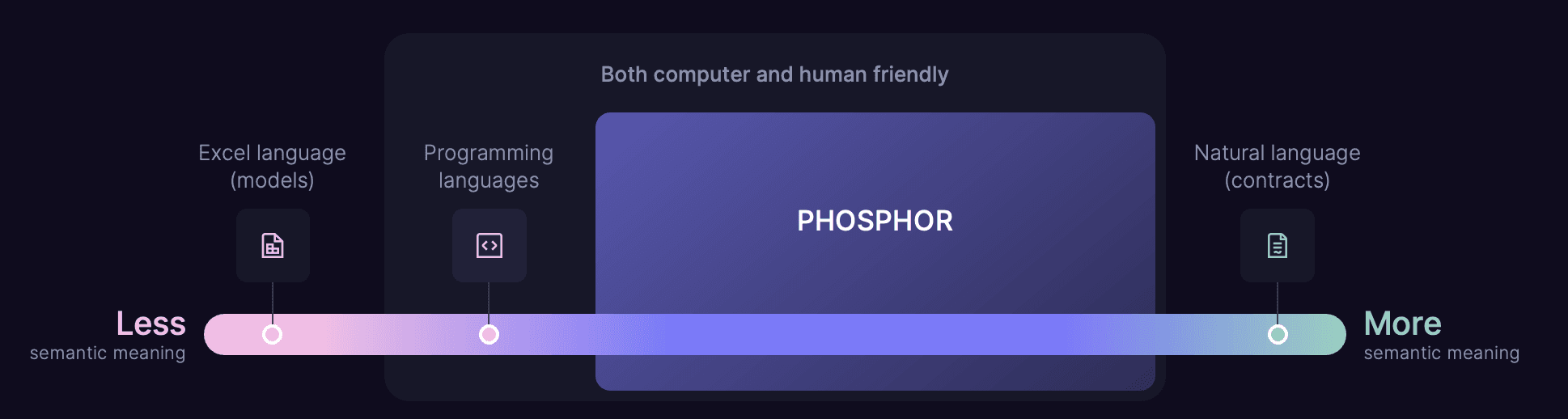

Charting these languages by their semantic capabilities is illuminating:

"Unstructured data" is practically synonymous with MS Word and Excel. This concern is often presented as a software problem.

But the real problem lies one step deeper: linguistics.

Computers can't handle ambiguity well. Programming languages that guide computers are constrained subsets of natural language. These constraints reduce ambiguity from natural language to enable a computer to compile to low-level machine instructions.

When language is ambiguous, compilation fails: the instructions are unclear.

To a computer, both Excel's cell reference language and the natural language of contracts are ambiguous beyond the files they're used within. They can't be compared by or connected to anything.

Charting these languages by their semantic capabilities is illuminating:

To the right, we see that natural language (contracts) has so much semantic meaning that a computer can't understand it. A question for thought: does contract logic require the full capabilities of the English language in the first place?

To the left, an absence of any meaning in Excel's reference language (=A5 * B9) eliminates all chance of connecting to systems or a basic ability to standardize, reuse and track changes against a knowledge baseline.

Notably, we place traditional programming languages to the left as well. These languages, used to create software or blockchain smart contracts, lack basic business-friendliness and require technical skills to adopt.

Phosphor's thesis is that a vast amount of space exists to create a digital language which:

Does not sacrifice the flexibility needed for these incredibly complex markets

Interoperates and provides superpowers for the existing paradigm as markets shift to new, more effective frameworks

Dramatically improves our ability to encode knowledge for reuse and reapplication to similar investments

To the right, we see that natural language (contracts) has so much semantic meaning that a computer can't understand it. A question for thought: does contract logic require the full capabilities of the English language in the first place?

To the left, an absence of any meaning in Excel's reference language (=A5 * B9) eliminates all chance of connecting to systems or a basic ability to standardize, reuse and track changes against a knowledge baseline.

Notably, we place traditional programming languages to the left as well. These languages, used to create software or blockchain smart contracts, lack basic business-friendliness and require technical skills to adopt.

Phosphor's thesis is that a vast amount of space exists to create a digital language which:

Does not sacrifice the flexibility needed for these incredibly complex markets

Interoperates and provides superpowers for the existing paradigm as markets shift to new, more effective frameworks

Dramatically improves our ability to encode knowledge for reuse and reapplication to similar investments

The questions we can only ask when this is solved

This paper has endeavored to take you from the cosmos of financial markets down to the atoms and bits of the assets that underpin them in order to crystallize the problem.

But the most interesting question is: what happens when this language problem becomes corrected? What does this new digital infrastructure enable?

Phosphor has been focused on this for years and we've uncovered opportunities that transform everything we thought was possible.

These are some of our bets for what’s to come:

Small asset owners and investors will soon be able to achieve terms and valuation in ways that have previously only been reserved for large, institutional portfolios.

Much of today’s proprietary expertise will become a market baseline tomorrow, enabling markets to concern themselves with a vastly more interesting set of problems.

Newly considered forms of legal contracts (which work with everyday case law) will steal much of the thunder from blockchain smart contracts. The immutable, unstoppable straitjacket of blockchain code is a tough sell in markets where optionality is required.

Digitization will take on scope in ways most haven’t fathomed. The combination of language-level adjustments with advances in AI unlocks technology options that boggle the mind and provide a real path to rapidly modernizing these systems at scale, unlocking value for asset owners along the way.

We have a wild vision for what this future looks like, and we’ve made huge strides toward it.

If you’re interested in learning more, email oliver@phosphor.co. It’d be a pleasure to hear from you!

This paper has endeavored to take you from the cosmos of financial markets down to the atoms and bits of the assets that underpin them in order to crystallize the problem.

But the most interesting question is: what happens when this language problem becomes corrected? What does this new digital infrastructure enable?

Phosphor has been focused on this for years and we've uncovered opportunities that transform everything we thought was possible.

These are some of our bets for what’s to come:

Small asset owners and investors will soon be able to achieve terms and valuation in ways that have previously only been reserved for large, institutional portfolios.

Much of today’s proprietary expertise will become a market baseline tomorrow, enabling markets to concern themselves with a vastly more interesting set of problems.

Newly considered forms of legal contracts (which work with everyday case law) will steal much of the thunder from blockchain smart contracts. The immutable, unstoppable straitjacket of blockchain code is a tough sell in markets where optionality is required.

Digitization will take on scope in ways most haven’t fathomed. The combination of language-level adjustments with advances in AI unlocks technology options that boggle the mind and provide a real path to rapidly modernizing these systems at scale, unlocking value for asset owners along the way.

We have a wild vision for what this future looks like, and we’ve made huge strides toward it.

If you’re interested in learning more, email oliver@phosphor.co. It’d be a pleasure to hear from you!

If you’re interested in connecting, email oliver@phosphor.co.

If you’re interested in connecting, email oliver@phosphor.co.

If you’re interested in connecting, email oliver@phosphor.co.

It’d be a pleasure to hear from you!

It’d be a pleasure to hear from you!

It’d be a pleasure to hear from you!